Submitted by Patrick on Thu, 08/01/2013 - 12:09pm

To great establishment fanfare, the Bipartisan Student Loan Certainty Act has now passed both Houses of Congress, and should be signed by President Obama shortly. Here's precisely how screwed students are. UPDATE: President Obama has signed the bill.

Submitted by Patrick on Tue, 03/05/2013 - 5:10pm

There's been quite a bit of chatter about the latest report on student loan debt out by the New York Federal Reserve Board. All the bad numbers are up: the total amount of student loan debt, the number of students taking out loans, and the number of those who have stopped repayment. But there's one figure that I haven't seen anybody really highlight, and it's the scariest. You can check out a PDF of the findings here.

Submitted by Patrick on Mon, 07/16/2012 - 2:17am

I recently sat down with The Daily Agenda to chat about student loan debt and how it relates to larger activist movements on- and off-campus.

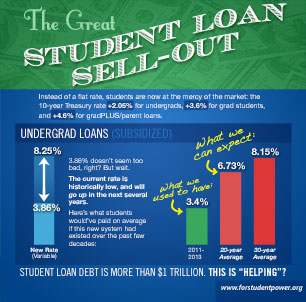

Submitted by Patrick on Wed, 08/31/2011 - 12:04am